'%3e%3cpath%20id='Vector'%20d='M13.334%203.95562L12.394%203.01562L4.66732%2010.7423V6.34896H3.33398V13.0156H10.0007V11.6823H5.60732L13.334%203.95562Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_63448'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.349121)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20id='Vector'%20d='M5.99996%204.07861V5.41195H10.3933L2.66663%2013.1386L3.60663%2014.0786L11.3333%206.35195V10.7453H12.6666V4.07861H5.99996Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_42480'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.745117)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Published 16:46 IST, June 13th 2024

Euro zone banks’ periphery premium is here to stay

Greece and Spain will grow at around 2% this year according to the International Monetary Fund, compared with 0.2% for Germany and 0.7% for France.

- Economy

- 3 min read

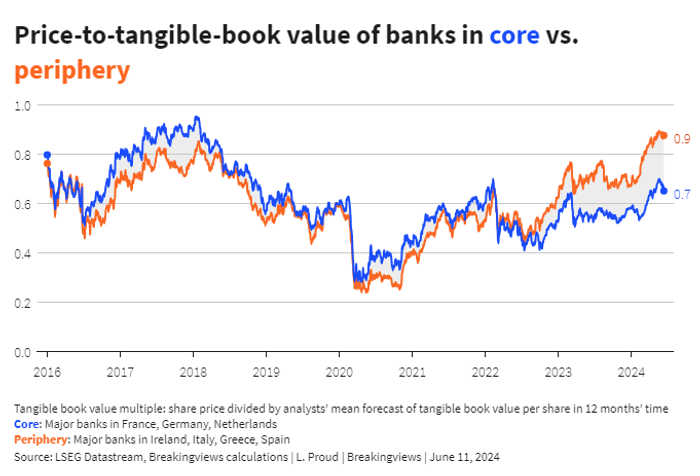

Rotten to the core. Banks in the euro zone periphery are once again at the centre of investors’ attention – but for a new reason. Lenders in Ireland, Italy, Greece and Spain on average trade at a roughly 30% valuation premium to those in so-called core countries like Germany, France and the Netherlands. The gap looks set to persist.

The core-periphery distinction describes the difference between a relatively cohesive central group of countries, led by Germany and France, and historically more volatile economies around the bloc’s edges. Many in the second group had to bail out their banking systems during the euro zone crisis of the 2010s. It’s surprising then that major lenders in those countries now leave French, German and Dutch lenders in the dust. On average, big banks in Ireland, Italy, Greece and Spain are worth 90% of forecast tangible book value in 12 months’ time compared with 70% for core-country banks, according to Breakingviews calculations using LSEG data.

Of the 23 major euro zone lenders that Breakingviews studied, nine of 10 highest-valued are based in the periphery, led by Madrid-based Bankinter and Italy’s 65 billion euro Intesa Sanpaolo. The National Bank of Greece, Dublin’s AIB Group and Bank of Ireland trade at roughly 90% or more of forecast tangible book. Paris-based BNP Paribas, at 65%, is behind two of the four big Greek banks – even though European supervisors have only just allowed Hellenic lenders to start paying dividends again.

The value gap partly reflects changing economic fortunes. Greece and Spain, for example, will grow at around 2% this year according to the International Monetary Fund, compared with 0.2% for Germany and 0.7% for France. President Emmanuel Macron’s decision on Sunday to call a snap election, a reaction to surging far-right support in France, underscores that political risks are increasingly present in the euro zone core.

Historic banking cleanups in the periphery also help. Governments helped lenders get rid of toxic assets. Greek banks’ non-performing loans to households fell from almost 50% of relevant exposures in 2017 to less than 10% in 2023, European Central Bank data shows. Past purges afforded some lenders a clean slate. Bank of Ireland and National Bank of Greece have emerged as relatively straightforward groups focused on key domestic businesses, and are forecast to generate 15% returns on tangible equity this year, using Visible Alpha consensus data.

Compare that with analysts’ 5% ROTE forecast for Deutsche Bank and 6% for Société Générale. German and French domestic lending may just be lower-returning businesses – a product of competition and regulation respectively. The core banks are also more biased towards investment banking, which tends to get a lower stock-market multiple. The problem for their shareholders is that there seems little reason for the periphery premium to disappear.

Context News

Shares in Société Générale fell 7.5% on June 10 after French President Emmanuel Macron called a snap parliamentary election. Local rival BNP Paribas fell 4.8% on the same day, while Crédit Agricole was down 3.6%. Macron on June 9 called snap legislative elections after his party was trounced in elections for the European Parliament by Marine Le Pen’s far-right National Rally. Macron said the EU result was grim for his government, and one he could not ignore. In an address to the nation, he said lower house elections would be called for June 30, with a second-round vote on July 7.

Updated 16:46 IST, June 13th 2024