'%3e%3cpath%20id='Vector'%20d='M5.99996%204.07861V5.41195H10.3933L2.66663%2013.1386L3.60663%2014.0786L11.3333%206.35195V10.7453H12.6666V4.07861H5.99996Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_42480'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.745117)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20id='Vector'%20d='M13.334%203.95562L12.394%203.01562L4.66732%2010.7423V6.34896H3.33398V13.0156H10.0007V11.6823H5.60732L13.334%203.95562Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_63448'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.349121)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Published 10:47 IST, October 11th 2024

What Masayoshi Son can teach us about investing

Son's rollercoaster career represents a case study for the original conundrum of active investing: is there really such a thing as skill, or is it just luck?

- Markets

- 6 min read

The Son also rises. When OpenAI raised $6.6 billion of fresh capital last week, the pioneering artificial intelligence startup’s implied $157 billion valuation was the headline-grabbing news. Yet squirreled away in its list of new shareholders was another surprising disclosure.

Investing alongside tech venture capitalist Thrive Capital, financial bluebloods like Khosla Ventures and Fidelity Management & Research, and heavyweight corporate partners such as Microsoft and Nvidia, was a $500 million contribution from SoftBank – the Japanese group synonymous with its eccentric founder Masayoshi Son.

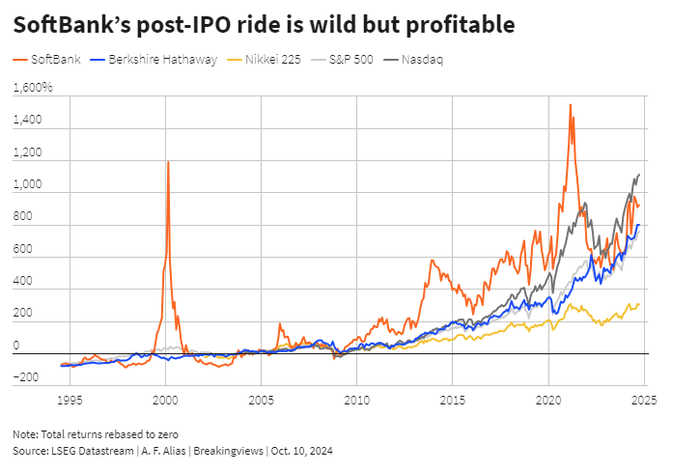

To say that opinions are divided on the value of a financial endorsement from SoftBank would be putting it mildly. Son is probably the most controversial venture capitalist the world has ever seen. His rollercoaster career represents a case study for the original conundrum of active investing: is there really such a thing as skill, or is it all just a matter of luck?

It is certainly easy to cast Son as essentially a high-stakes punter. A gripping new biography by Lionel Barber, the former editor of the Financial Times, does just that. The clue is in the title: “Gambling Man: The Wild Ride of Japan’s Masayoshi Son”.

Exhibit one is Son’s investment track record, which is decidedly up and down. On the positive side of the ledger, he spotted the potential in search engine Yahoo when the dotcom boom was in its early stages and bought 30% of Alibaba for a paltry $20 million on the strength of a six-minute meeting with Jack Ma, the Chinese e-commerce group’s founder, in 1999. On the negative side, he sank $14 billion into Adam Neumann’s office-sharing startup WeWork prior to its spectacular collapse in 2019. (“It was like feeding a monkey alcohol” is how Barber reports one of Son’s investors ruefully remembering the partnership.) He also lost $1.5 billion betting on Lex Greensill, the Australian watermelon-farmer turned globe-trotting financial alchemist whose eponymous supply chain finance firm blew up in 2021.

Then there is the lingering suspicion that, for all the appearance of technological prescience and stock-picking savvy, Son’s success was really due to massive macroeconomic tailwinds. On this view, SoftBank’s early home runs in U.S. tech were just down to the strength of the Japanese yen in the mid-1990s. When the dollar subsequently recovered, any Japanese investments stateside enjoyed a stonking foreign-exchange gain. In the 2000s, meanwhile, the Bank of Japan was the first monetary authority to pin its policy rate at zero. It is easier to make successful investments when funding is virtually free.

Son’s fondness for leverage is widely held to be another symptom of a chancer. Barber captures SoftBank’s dependence on debt in his account of Son’s only meeting with Warren Buffett. In 2017, the Japanese executive flew 6,000 miles to Berkshire Hathaway’s headquarters to persuade the legendary investor to back SoftBank’s $100 billion Vision Fund. The pitch lasted barely 20 minutes. “I’m a cash-flow guy” was Buffett’s laconic response.

Yet the story is not so straightforward. For a start, it is vital to remember how venture capital works. Most new companies fail, wiping out their financial supporters in the process. The skill is ensuring the firms that survive multiply their value 10 or a hundred times. Judged by this standard, Son is hardly a slouch. His four-decade streak may have been built on picking only a handful of winners amid an army of duds. But the winners really won.

It is true that Son’s successes rode broader macroeconomic waves. But his edge has been precisely to identify secular trends such as the explosive growth of personal computing in the 1990s, Japanese broadband in the 2000s, and Chinese e-commerce in the 2010s, and then to back a slate of companies that stand a chance of benefiting from the shift. In investment terms, Son understands that trend-picking is as valuable as stock-picking, if the trend is big enough.

Son’s approach is the antithesis of Buffett’s. The Sage of Omaha is famous for his devotion to businesses with robust and durable defences against competition. SoftBank by contrast has prided itself on shameless replication. It was by ruthlessly transplanting successful American businesses such as financial data firm Morningstar and online broker E*Trade that Son ended up controlling 70% of Japan’s internet economy.

While Buffett is famously allergic to overpaying for investments, Son sees it as a means to an end. His first big coup in the United States was paying more than double the asking price for the country’s largest computer convention from Las Vegas mogul Sheldon Adelson in 1993. When the internet took off, the deal no longer looked so dumb. “Sheldon played checkers,” Adelson’s right-hand man reflected later, “Masa played chess.”

Behind the suspicion of Son is the mistaken belief that all investment skill is a temporary sham. The efficient-market hypothesis, which mistakenly posits that it is impossible to consistently beat the market, and the relentless rise of index-tracking exchange-traded funds have induced a deep crisis of confidence in active investors. Many find it hard to accept that great venture capital managers need a creative streak. Part of the skill in backing startup companies, however, is precisely that you make your own luck.

In 2016, SoftBank acquired Arm, the global leader in chip design. In July it snapped up Graphcore, a struggling British AI chipmaker once billed as a competitor to $3 trillion Nvidia. With his investment in OpenAI, Son’s next big bet – on the prospects of generative AI – is taking shape. Given that Son sold SoftBank’s Nvidia shares in 2019, thereby missing much of the AI chip giant’s meteoric rise, is this just another throw of the dice from the reckless “Gambling Man”?

Back in 2001, Son told Sir Peter Bonfield, then chief executive of UK telecom operator BT, that he planned to build a leading Japanese broadband provider from scratch by slashing prices in half. Bonfield was baffled: who wins by selling at a loss? Within three years, SoftBank was one of the top three broadband providers in the world’s second largest economy. As Barber writes, “Masa had grasped the new economics of the digital revolution far earlier than rivals.” Bonfield’s verdict was even simpler: “He was right and we were wrong.”

Sceptics of Son’s latest adventure – and of active fund management generally – might want to take note.

Updated 10:47 IST, October 11th 2024