'%3e%3cpath%20id='Vector'%20d='M13.334%203.95562L12.394%203.01562L4.66732%2010.7423V6.34896H3.33398V13.0156H10.0007V11.6823H5.60732L13.334%203.95562Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_63448'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.349121)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20id='Vector'%20d='M5.99996%204.07861V5.41195H10.3933L2.66663%2013.1386L3.60663%2014.0786L11.3333%206.35195V10.7453H12.6666V4.07861H5.99996Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_42480'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.745117)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Published 15:11 IST, June 12th 2024

Spain’s $24 bln investment giant has too many hats

Criteria Caixa, the investment arm of the Spanish La Caixa foundation, will present a new strategic plan on June 17.

- Markets

- 6 min read

Master of none.

One of the biggest players in Spanish M&A right now is also one of the most unusual. Criteria Caixa, the 22 billion euro ($24 billion) investment arm of the La Caixa charitable foundation, has been snapping up stakes in listed companies while also making its presence felt at local blue chips Telefónica and Naturgy Energy Group. The group will present a new strategic plan in Barcelona on June 17, a person familiar with the matter told Breakingviews.

Criteria’s Chair Isidro Fainé seems fixated on protecting national champions from foreign incursions, which could chill Spanish M&A. One fresh example occurred on Monday, when Abu Dhabi’s TAQA dropped its takeover bid for Spanish utility Naturgy, sending the shares down more than a tenth. The informal political mission is also at odds with the group’s official one of preserving and growing the wealth of its parent charity.

The organisation’s roots date back to the founding of a Barcelona-based savings institution in 1904 by Catalan lawyer Francesc Moragas. A charitable arm, retail bank and investment holding company for many years all sat under one roof, until a series of reorganisations starting in the 2000s. The group’s managers, including Fainé, eventually carved it into three parts: the La Caixa philanthropic foundation, which fully owns the investment wing Criteria Caixa, which in turn owns a portfolio of stocks including a one-third stake in 39 billion euro Spanish lender CaixaBank. Fainé chairs the foundation and the investor, but stepped down as head of CaixaBank’s board in 2016.

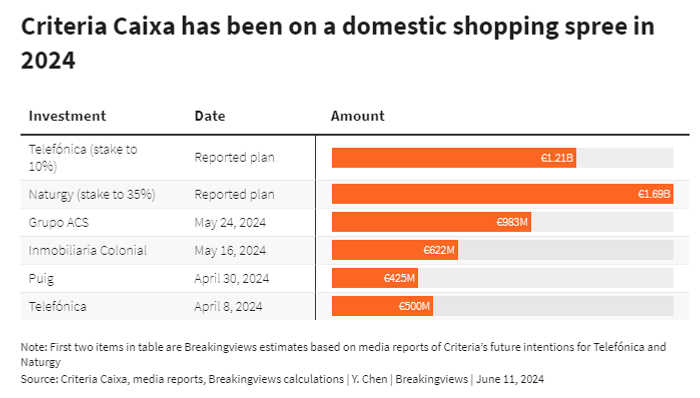

After a few years of focusing on debt reduction, Criteria now seems to be in expansion mode. Fainé’s new CEO Ángel Simón at Criteria started his job in February and quickly embarked on a buying spree, pocketing 2.5 billion euros’ worth of stakes in listed companies during April and May, according to Breakingviews calculations. That includes chipping in on Spanish fashion house Puig’s initial public offering, buying a 9% holding in Spanish construction company Grupo ACS, almost doubling its stake in Spanish telecom giant Telefónica to 5%, and raising its stake in property group Inmobiliaria Colonial to 17%.

That’s not all. Criteria is also mulling increasing its Telefónica holding to 10%, a source familiar with the matter told Breakingviews, and was planning on boosting its ownership in Naturgy from 27% to around 35% as part of a joint takeover with TAQA. It’s unclear whether that idea will go ahead now that the joint takeover is off. But those two deals would cost 2.9 billion euros in total, taking the possible overall spending this year to 5.4 billion euros, based on Breakingviews estimates.

The spree makes life tricky for Spanish M&A bankers, who are trying to figure out which foreign takeovers are likely to fly in Madrid. Criteria claims to be non-political, but from the outside Fainé seems to be in sync with the government. The group has been upping its stake in Telefónica alongside state fund SEPI, helping Fainé’s group earn the nickname “private SEPI” among Spanish financiers. The pair acted shortly after a move by Saudi Telecom Company, which last September said it had bought 4.9% of the Spanish telco’s shares and financial instruments giving it another 5% economic exposure.

At both Telefónica and Naturgy, where big private equity shareholders are looking to exit, Criteria wants to help stabilise the companies’ ownership while boosting its managerial presence, a person familiar with the strategy told Breakingviews. The problem is that it looks increasingly difficult to judge what exactly Fainé is after. In April, for example, newspaper Expansión reported that Criteria would consider putting a bid together to counteract a politically controversial Hungarian offer for train maker Talgo. Fainé may see it as a matter of reputation and influence. The risk is that he ends up moonlighting for the Spanish government, but without the legal certainty or accountability of formal state M&A intervention.

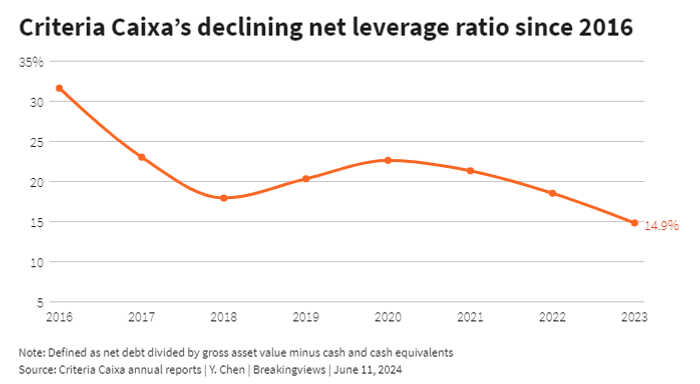

The other problem with Criteria’s deal spree is financial. It’s not clear how Fainé and Simón are funding the splurge, but there are few good options. Having managed to more than halve its net borrowings to 15% of total asset value in 2023 from 32% in 2016, the group risks undoing much of that progress if it uses debt. Its credit is rated as BBB+ by Fitch and Baa2 by Moody’s – three and two notches respectively above junk.

Selling down stakes would be another possibility. For example, Criteria on Tuesday said it had offloaded about 600 million euros of shares in mobile tower group Cellnex. But that holding is small relative to its 12.1 billion euro CaixaBank stake and 5.5 billion euro Naturgy one. Selling either of those would raise issues. The utility is a tough selldown target because of the takeover drama and the lender hard to offload too because of its role as a healthy dividend payer. Criteria should get about 1 billion euros from CaixaBank’s 2024 dividend alone, according to Breakingviews calculations using Visible Alpha data. That incoming cash will admittedly help reduce leverage at the margin, but a big chunk of it gets earmarked for the so-called “social dividend” to the La Caixa parent foundation. The payment was 400 million euros last year and is set to rise this year as the foundation budgeted a record 600 million euros for social spending.

Finally, it’s unclear how Fainé and Criteria’s M&A activism are supposed to fit with its core mission: to “preserve and grow” the La Caixa foundation’s wealth. Taken at face value, that would imply avoiding Spanish stocks, since the IBEX 35 Index has delivered a 50% total return including reinvested dividends over the past decade compared with 140% for the MSCI All Country World Index and 230% for the S&P 500 Index. The investment arms of other non-profits, like Britain’s Wellcome Trust or U.S. university endowment funds, have become sophisticated international players, investing outside their home markets and in alternative assets like private capital. The logic in these cases is that optimising for anything but financial returns means short-changing the foundation.

Fainé and Criteria clearly don’t see it that way. But if their protectionist M&A binge ends up delivering subpar returns, it won’t just be M&A bankers that have cause for complaint.

Context News

Criteria Caixa, the investment arm of the Spanish La Caixa foundation, will present a new strategic plan on June 17, according to a person familiar with the matter. Criteria Caixa said on June 10 that it had not reached an agreement with Abu Dhabi’s TAQA over a potential joint takeover bid for Spanish gas firm Naturgy Energy Group. TAQA said in April that it was in talks with Naturgy’s three largest shareholders – Criteria and private equity funds CVC Capital Partners and Global Infrastructure Partners, which own 27%, 21% and 21% respectively, according to LSEG data. Criteria said it will continue to explore alternatives to accelerate Naturgy’s growth, provide stability to the company’s shareholder register and allow Criteria to maintain its position as a partner to the company.

Updated 15:24 IST, June 12th 2024