'%3e%3cpath%20id='Vector'%20d='M5.99996%204.07861V5.41195H10.3933L2.66663%2013.1386L3.60663%2014.0786L11.3333%206.35195V10.7453H12.6666V4.07861H5.99996Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_42480'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.745117)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20id='Vector'%20d='M13.334%203.95562L12.394%203.01562L4.66732%2010.7423V6.34896H3.33398V13.0156H10.0007V11.6823H5.60732L13.334%203.95562Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_63448'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.349121)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Published 14:13 IST, October 18th 2024

Inflation is not dead, it’s just resting

There’s a long history of monetary policymakers prematurely celebrating the end of inflation, only to be caught off guard by its sudden resurgence.

- Economy

- 6 min read

Ceased to be. Over the past three years inflation has gone from “transitory” to “persistent” to, well, boring. Across the developed world annual price increases are returning towards the subdued 2% level targeted by many central banks. Commentators are talking of the Goldilocks scenario, where the economy, like the porridge in the fairy tale, is neither too hot nor too cold.

Don’t break out the champagne yet, though. There’s a long history of monetary policymakers prematurely celebrating the end of inflation, only to be caught off guard by its sudden resurgence. Perhaps the best example comes from the early 1970s.

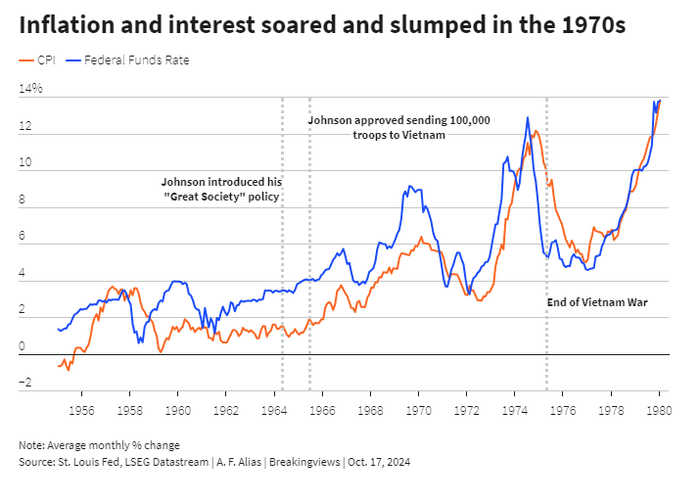

Inflation in the United States picked up in the late 1960s in the wake of the Vietnam War and spending on President Lyndon Johnson’s “Great Society” set of social programs. The Federal Reserve responded by raising interest rates to near 10% in 1969. There followed a brief recession and a stock market collapse. Inflation receded, falling to 2.7% by 1971 – close to its current level. By the end of the year, the Fed’s official policy rate was back at 3%. Large-cap stocks boomed. Then all hell broke loose. In 1974 inflation hit 10%, interest rates peaked at over 13%, the “Nifty Fifty” stocks collapsed, and a severe recession ensued.

There are several factors which help explain the dramatic resurgence of inflation. In 1971 the dollar lost its monetary anchor after President Richard Nixon closed the so-called Gold Window, ending the convertibility of the U.S. dollar into the precious metal. At the same time, Nixon was putting pressure on Fed Chair Arthur Burns to pump up the U.S. economy during his successful 1972 re-election campaign. Both Nixon and Burns prioritised low unemployment over price stability. The following year, OPEC imposed an embargo on oil-importing countries that had supported Israel during the Yom Kippur War. The price of the black stuff tripled.

The Fed initially accommodated the energy crisis by cutting interest rates. The economist Milton Friedman and others later criticised that action. Yet had the U.S. central bank prevented other prices from rising it’s possible the entire economy would have collapsed. Besides, a recent International Monetary Fund study finds that historical instances of “unresolved” inflation are often associated with energy shocks.

In their 1983 book, “Is Inflation Ending: Are You Ready?” A. Gary Shilling and Kiril Sokoloff pointed to several other factors pushing up prices. These included support schemes for farm and dairy produce as well as tariffs on sugar and Japanese steel. A proliferation of regulations increased the costs of doing business. In 1971 Nixon introduced controls on prices and incomes, which predictably failed to stem the inflation tide. Cost of living adjustments to social security payments and the minimum wage insulated much of the American population from the ravages of inflation. Workers went on strike to maintain their wage differentials. Productivity growth was cut in half. The weak dollar pushed up import prices. Most of these inflationary forces were self-reinforcing.

Shilling and Sokoloff describe a historical link between the rising government share of the economic pie, which reached around 40% of U.S. GDP in 1980, and spiralling prices. The central bank played a supporting role. After he stepped down in 1978, Burns lamented that the “Federal Reserve was itself caught up in the philosophic and political currents that were transforming American life and culture.” By then, however, Americans were more worried about inflation than job losses. Under Chair Paul Volcker the central bank received a mandate to squeeze inflation out of the system, a feat achieved with sky-high interest rates, two severe recessions and soaring unemployment.

Today is not 1973 redux. Still, there are some interesting similarities. The thicket of government regulations gets ever thicker. China and the other members of the so-called “Global South” of developing countries are hatching plans to break the U.S. dollar’s grip on the international monetary system. Inflation-busting pay rises continue to make headlines. Earlier this month, U.S. dockworkers ended their strike after receiving a 62% pay hike. Boeing employees have rejected an offer of a 30% raise from the troubled aircraft manufacturer. Vice President Kamala Harris promises a crackdown on corporate price-gouging if she wins next month’s presidential election, which to some sounds suspiciously like the reimposition of price controls. Her opponent, Donald Trump, wants hefty tariffs on imported goods with an additional penalty on Chinese imports.

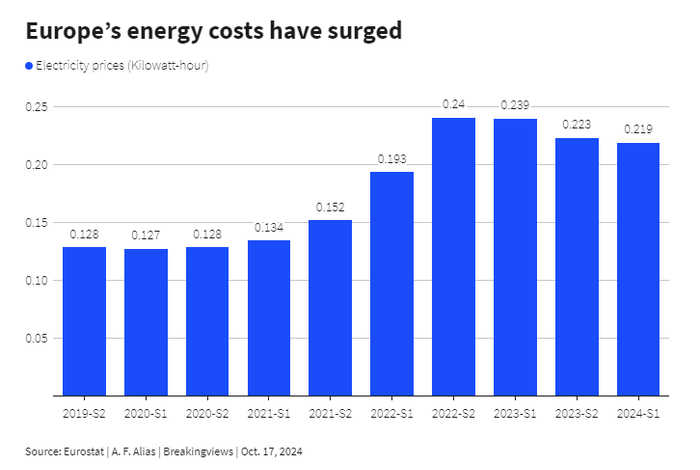

Meanwhile, another war is roiling the Middle East. Even if it does not immediately cut off oil supplies in the Gulf, there’s still a question mark over the sustainability of oil supplies in the medium term. Exxon Mobil has warned of potential oil shortages by 2030 due to inadequate new investment – though the International Energy Agency disagrees. The shift to renewable energy has helped to push up the cost of electricity in the European Union by 45% since 2020, according to Eurostat. As in the 1970s, higher energy costs – exacerbated by Russia’s war with Ukraine - are rendering obsolete much of Europe’s manufacturing base. German industrial production is down 14% since its 2017 peak, according to Andy Lees of MacroStrategy Partnership.

Public debt is much larger than five decades ago. The IMF expects total government debt to reach $100 trillion by the end of this year. Last year, the U.S. fiscal deficit amounted to $1.6 trillion or 6.3% of GDP . John Cochrane of Stanford University, whose “fiscal theory” posits a connection between excessive government spending and inflation, believes it’s not a question of whether inflation returns, but when.

Sokoloff, the founder and chairman of investment adviser 13D Research & Strategy, successfully called the turn in inflation forty years ago. He’s not so sanguine today. What we’re seeing, in his view, is a cyclical downturn. Enormous secular drivers of higher prices remain in place. Deglobalisation, rearmament, de-dollarisation, aging demographics, climate change and the energy transition will continue to put upward pressure on inflation over the coming years. As in the early 1970s, there’s no political appetite for high real interest rates to keep a lid on prices or austerity to bring government finances under control.

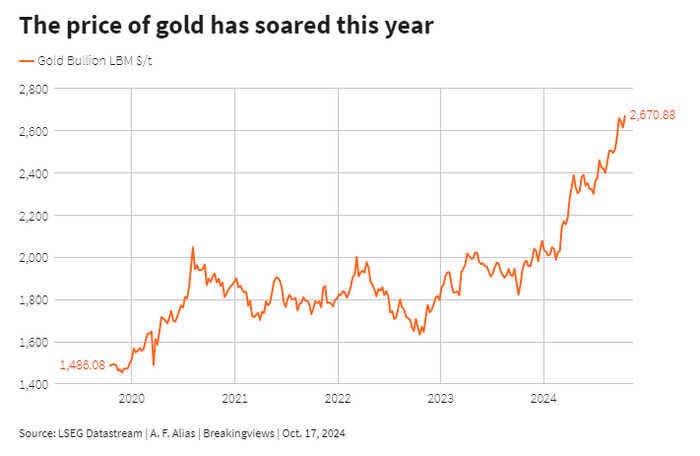

Gold, Sokoloff says, has long been a reliable barometer of both inflation and deflation. Since the start of the year the price of the yellow metal has risen nearly 30%. It’s telling us, says the veteran analyst, that four decades of disinflation are over and bonds are now in a long-term secular bear market. Inflation is not dead, just resting.

Updated 14:13 IST, October 18th 2024