'%3e%3cpath%20id='Vector'%20d='M5.99996%204.07861V5.41195H10.3933L2.66663%2013.1386L3.60663%2014.0786L11.3333%206.35195V10.7453H12.6666V4.07861H5.99996Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_42480'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.745117)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20id='Vector'%20d='M13.334%203.95562L12.394%203.01562L4.66732%2010.7423V6.34896H3.33398V13.0156H10.0007V11.6823H5.60732L13.334%203.95562Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_63448'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.349121)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Published 08:39 IST, September 11th 2024

China’s banks have a nasty case of indigestion

The problem is, asking China’s official data collectors about bad debt is like asking a dyspeptic patient how much junk food they really eat.

- Economy

- 6 min read

Overserved. China's financial sector has serious heartburn. For decades, Beijing has leaned on its state-controlled banks to turbo-charge growth by extending credit. But lenders are now clogged with risky assets. The result is something like indigestion: not critical, but painful for the $17 trillion economy.

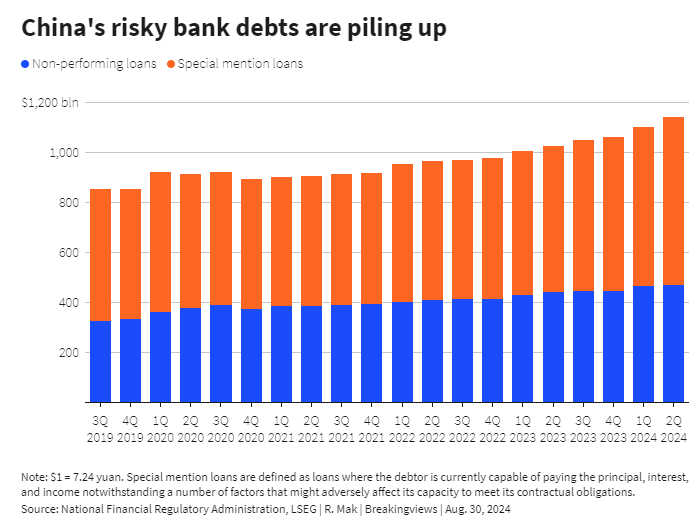

On paper, the country's banks look remarkably healthy given 2020's twin shocks of the pandemic and a burst property bubble. Official data show them sitting on 3.3 trillion yuan, roughly $460 billion, of non-performing loans. Add in another $670 billion of less-problematic-but-still-pesky "special mention" loans, which include credit extended to struggling property developers and cash-strapped local governments, and it doesn’t even reach 4% of their aggregate lending.

The problem is, asking China’s official data collectors about bad debt is like asking a dyspeptic patient how much junk food they really eat. Other sources take a gloomier view. Bad loans in the property sector today alone could be over $1 trillion, reckons research firm GavekalDragonomics.

Even so, the chances of a chaotic implosion of China's tightly-controlled financial system are extremely low. China's four biggest lenders - Industrial and Commercial Bank of China, Bank of China, China Construction Bank and Agricultural Bank of China - are all state owned and too big to fail in every way. Moreover, regulators and bank executives have spent years devising ways to manage the bad debt problem, and while that system is strained, it still more or less works.

THREE-COURSE PROBLEM

Think of the sector's problem assets as coming in three distinct flavours. The least unpalatable are loans are mostly politically connected ones from local government financing vehicles, or LGFVs - the 3,000-plus entities created by local governments mainly to fund infrastructure projects. Last year, LGFV debt topped $8.5 trillion, according to the International Monetary Fund. Fitch Ratings estimates credit provided to LGFVs could account for up to 17% of total assets at the banks it covers.

Because of the political nature, lenders have little choice but to keep rolling over that kind of debt before it comes due for repayment. Zunyi Road and Bridge Construction, an LGFV based in Guizhou province, received a 20-year extension on a $2 billion loan with the interest rates halved, local media reported. Not all of the projects these loans finance are duds; LGFVs also fund useful infrastructure like metro stations. But helping them out eats into banks’ profitability. Under a severe stress scenario where 15% of LGFV loans are renegotiated, bank sector profits would decrease by 6%, estimates asset manager Pimco.

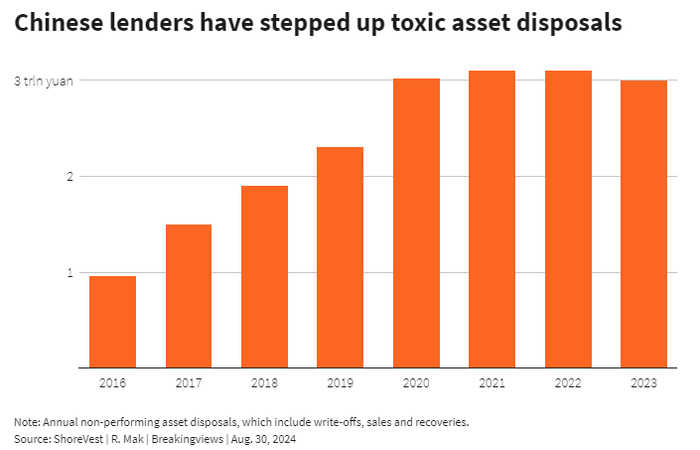

That’s disagreeable but not terminal. Larger and well-capitalised banks can take the earnings hit, though shakier regional and rural banks will require some combination of government bailouts and consolidation. And some bad loans may yet come good. As for the other two flavours of bad debt, banks are likely to try and get these out of their system one way or another. Over the past few years, lenders have stepped up the pace of bad asset disposals, which since 2020 have surpassed 3 trillion yuan a year, or nearly 3% of GDP , according to researcher Dinny McMahon at Trivium.

The first category are assets that can be sold, auctioned or securitised. China's bankruptcy process is still underdeveloped, and onerous restrictions and lengthy court settlements mean it's still more efficient for banks to directly offload toxic loans to mostly state-backed investment vehicles known as “asset management companies”, even at a loss. Standard Chartered-backed China Bohai Bank, for instance, plans to sell assets worth 29 billion yuan at an up to 40% discount, which will result in a financial hit equivalent to more than three-quarters of its 2023 earnings.

Asset management companies are themselves overstretched in many cases, so often act more like a clearinghouse than an investor, selling on the loans they buy to specialist funds like ShoreVest. These investors can make double-digit returns from underlying collateral. Despite slumping real estate values, logistics warehouses and shopping malls across the country, for instance, are still generating cash, according to ShoreVest founder Benjamin Fanger.

The remaining group of loans are those where banks will try to recover the outstanding amount themselves, and tap provisions to cover any outstanding losses. These write-offs totalled 1.3 trillion yuan last year, per GaveKal. Lenders like Ping An Bank have beefed up in-house capabilities to collect on delinquent credit card dues, mortgages and such.

Diner's Remorse

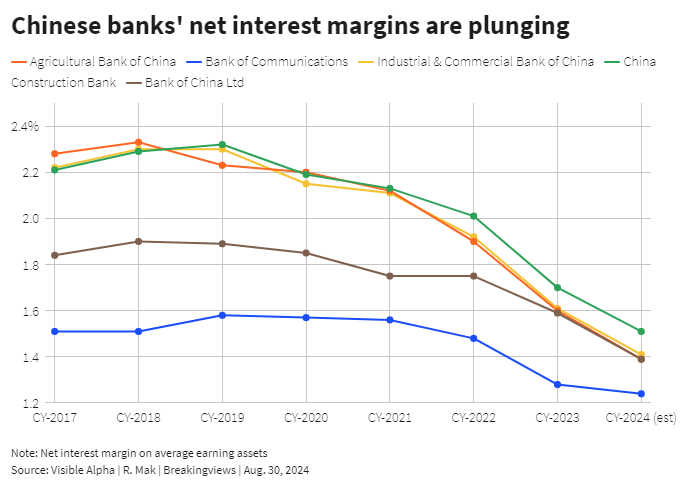

Through warehousing, selling and writing off loans, China's banks are muddling through. But not without cost. Profitability is being squeezed amid sluggish credit demand, interest rate cuts and Beijing's calls for lenders to funnel cheap credit into strategic sectors. Average net interest margins at the big four, plus number-five lender Bank of Communications, are forecast to fall to 1.4% this year, from over 2% in 2019, according to Visible Alpha; As a result, the average return on equity is expected to fall to 8.6% from 10% over the same period.

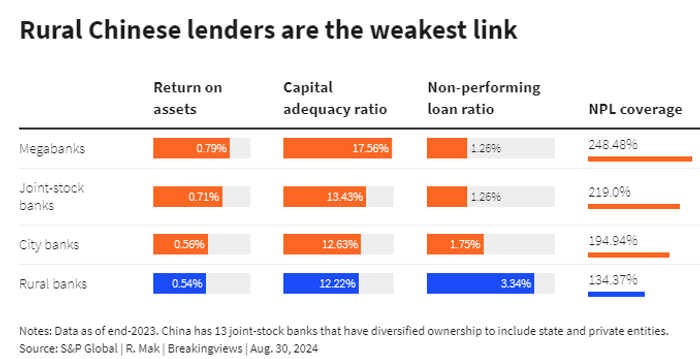

Because Chinese banks are required to set aside capital to cover losses from write-offs, a shrinking bottom line will make it harder to maintain the current pace of asset disposals, notably at rural commercial lenders, which make up 14% of all Chinese bank assets. They have the lowest profitability but the highest non-performing loan ratios. Large-scale recapitalisation, which can mean local governments issuing bonds for the purpose, may be required.

The bigger concern for Beijing's economic planners is how to prop up economic expansion. For past two decades, the country has relied on investment-driven growth by allocating credit to state and privately-owned firms. That is no longer possible: using historical data on nominal GDP growth created from loans, and assuming banks maintain a 30% dividend payout ratio, JPMorgan analysts calculate that banks would need more than a 10% return on equity to generate enough capital that they can help the government hit its economic expansion target this year.

Pumping out debt isn’t the only way to get growth. China for years has sought ways to stoke domestic consumption. That is probably the next chapter for China's economy. In the meantime, the stakes are rising. If consumers don’t pick up the slack, the economy slows, bad debts are likely to rise even further, and a nasty case of financial dyspepsia will turn into something worse.

Updated 08:39 IST, September 11th 2024