'%3e%3cpath%20id='Vector'%20d='M5.99996%204.07861V5.41195H10.3933L2.66663%2013.1386L3.60663%2014.0786L11.3333%206.35195V10.7453H12.6666V4.07861H5.99996Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_42480'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.745117)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20id='Vector'%20d='M13.334%203.95562L12.394%203.01562L4.66732%2010.7423V6.34896H3.33398V13.0156H10.0007V11.6823H5.60732L13.334%203.95562Z'%20fill='black'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_2043_63448'%3e%3crect%20width='16'%20height='16'%20fill='white'%20transform='translate(0%200.349121)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Published 13:54 IST, October 4th 2024

China and India reveal emerging market mistakes

The very word “emerging” suggests that less-developed economies with strong growth prospects can be expected to deliver superior investment returns.

- Markets

- 6 min read

Tiger trap. Investors make two profound errors in their approach to emerging markets. First, they are entranced by GDP growth even though there is no evidence of a positive correlation between an expanding economy and stock market returns. Second, they assume that valuations are a reliable predictor of returns. The strong outperformance of Indian stocks relative to Chinese equities since the financial crisis of 2008 shows how wrong this approach has been.

The very word “emerging” suggests that less-developed economies with strong growth prospects can be expected to deliver superior investment returns. Let’s see how that turned out. Over the past 15 years, the Chinese and Indian economies have both grown rapidly. China’s GDP expanded by roughly 2% a year more than India’s, when measured in constant U.S. dollars. Back in September 2009, the price-to-earnings multiple of the MSCI China Index was 25% lower than for MSCI India Index. Yet despite starting out cheaper and experiencing faster economic growth, the Chinese stock market since 2014 has delivered total annual returns of just 2.5% in dollar terms. Indian stocks have compounded annually by four times that amount, according to Jefferies.

There’s a relatively simple explanation for this divergence. In late 2008, the Chinese government in Beijing launched a huge stimulus to stave off the global financial crisis. It used the country’s vast domestic savings to finance an extraordinary investment boom. Gross domestic fixed capital formation soared from 38% to 44% of GDP and has remained elevated. The investment splurge was accompanied by rapid credit growth and supported by easy money. By contrast, India had relatively low savings and investment. Between 2009 and 2020, investment fell from 34% to 27% of GDP. Indian interest rates on average were twice as high China’s.

Economic theory posits that the return on capital should eventually equal its cost. Sure enough, China’s low cost of capital has delivered meagre returns. Capital has been misallocated on a grand scale, as evidenced by chronic levels of excess capacity across the economy. Since its housing bubble burst in 2020, the People’s Republic has been beset by debt deflation. India enjoyed no real estate, credit or investment boom and thus avoided the ensuing hangover. Its relatively high cost of capital produced relatively high returns on investment.

This macroeconomic analysis is evident in the reports and accounts of listed Chinese and Indian companies. One gauge of whether a company is investing prudently is the ratio of new capital expenditure to depreciation on past investments. Gillem Tulloch, founder of Hong Kong-based GMT Research, has examined the returns of Chinese and Indian companies which have a minimum of 10 years of data, which equates to about a quarter of the listed firms in both markets. In 2014, the average capex for Chinese public companies was 2.3 times depreciation. The ratio for their Indian counterparts was considerably lower, at 1.5 times. Since then, Chinese firms have consistently invested more than their Indian counterparts.

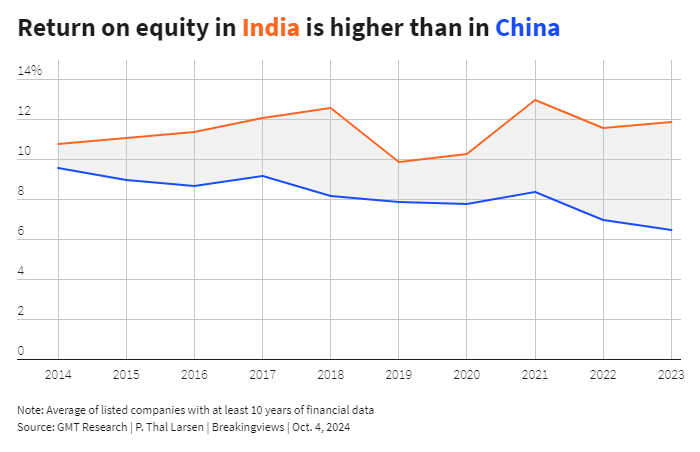

A key component of profitability is measured by the ratio of a company’s sales to its total assets. More efficient businesses have a higher level of asset turnover. Tulloch finds that this measure in India averaged around 1 times over the past decade. The average Chinese company, on the other hand, recorded sales relative to its assets of half that level. As a result, the return on equity (ROE) of Indian companies between 2014 and 2023 remained stable in the range of 10% to 13%, while the average ROE in China fell from 10% to 6% over the same period, according to Tulloch.

Since investment returns have lagged economic growth, Chinese firms have had to raise more capital, thereby diluting existing shareholders. The total number of shares in the MSCI China Index has increased by 2.5 times since 2014, according to CLSA. Yet earnings per share have scarcely budged. Investors have taken notice. The valuation of the Chinese benchmark has declined from over 2.5 times book value in 2020 to 1.3 times earlier this year. Meanwhile, the price-to-book ratio for MSCI India Index, which averaged just over 3 times over the last decade, has risen to 4.5 times.

Alex Duffy, an emerging markets specialist at Marathon Asset Management, argues that India’s capital discipline is starting to break down. Indian companies are currently adding new capacity across a variety of sectors, including steel, cement and power generation. Jefferies expects India’s investment share of GDP to rise from a low of 28.5% to 33% over the next three years. High stock market valuations have attracted a flood of initial public offerings. Private investment funding by banks and other financial institutions has nearly doubled since 2022, according to Jefferies.

Retail investors have helped to push the valuations of Indian midcap stocks to 35 times forecast earnings, a 70% premium to their long-term average, with no discernible improvement in growth rates or underlying profitability, says Duffy.

While India’s stock market is showing signs of a speculative blow-off, China’s capital cycle may be approaching a trough. Chinese companies’ capex to depreciation ratio has dipped to 1.5 times, in line with Indian levels, according to Tulloch. Private market capital raisings are down 98% from the pre-Covid-19 period, says Duffy. The securities regulator has instructed listed firms to increase their distributions to shareholders. Share buybacks now account for nearly 40% of total payouts. As stock repurchases have risen, the number of outstanding shares has started to fall, according to CLSA. In principle, a declining share count should boost growth in earnings per share.

Since Beijing unveiled a new stimulus package last week, Chinese stocks have been on a tear. The People’s Bank of China promises to provide loans for companies to repurchase more shares. That’s not enough. Chinese industry needs to remove excess capacity, says Duffy. It’s unclear whether President Xi Jinping has got the message. Chinese investment may have declined as a share of GDP but is still a heady 42%. Chinese stocks may still appear cheap on every valuation measure. However, until there is clear evidence of retrenchment on the supply side, emerging market investors should remain wary.

Updated 13:54 IST, October 4th 2024